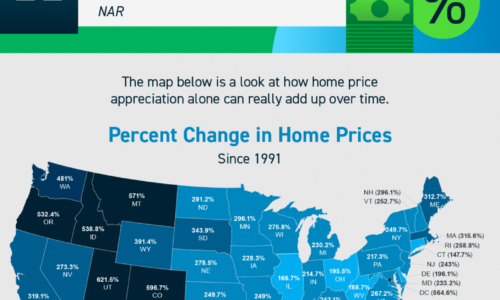

Homeownership Wins Over Time [INFOGRAPHIC] Some Highlights If you’re questioning whether or not to buy a home this year due to today’s cooling market, consider the long-term financial benefits of homeownership. As a homeowner, equity increases your wealth. On average, nationwide, home prices appreciated by 2% since 1991. Homeownership wins in the long run. If you’re ready to buy a home, […]

Do You Believe Homeownership Is Out of Reach? Maybe It Doesn’t Have To Be.

Do You Believe Homeownership Is Out of Reach? Maybe It Doesn’t Have To Be.

It turns out, millennials aren’t the renter generation after all. The 2022 Consumer Insights Report from Mynd says there’s a portion of millennial and Gen Z buyers who are pursuing homeownership as a way to build their wealth, but it may not be exactly the way previous generations have done it. The study explains how they’re breaking into the market:

“. . . younger generations of Americans are not buying into that dream in the same way that older generations have. A growing number of Americans are choosing to make their first real estate purchase as an investment property.”

Instead of buying a home and moving into it themselves, some young buyers are purchasing a home so they can use it as a rental. This tactic may be gaining popularity, at least in part, because of the affordability challenges brought about by today’s higher mortgage rates. The report above mentions how many people in this group are considering this approach. It says:

“Almost half of Millennials and Gen Z (43%) are considering buying an investment property compared to only 9% of Baby Boomers and 27% of Gen X.”

Why Younger Buyers Are Buying a Home To Use as a Rental

This strategy allows buyers to continue living in their current location, like the bustle of a city apartment or a neighborhood that they know and love, where they couldn’t afford to buy. But instead of giving up on the idea of owning a home, they buy a home in a more affordable area with the intention of renting it out.

In a way, they’re getting the best of both worlds. They live where they want, and they still own a home where they can afford it.

Their goal is to generate passive income and diversify their assets. It works like this: in addition to having a rental stream of income, the equity they build in their house will also help grow their net worth over time.

Bottom Line

If you’re thinking about buying a home as an investment strategy to build your wealth, let’s connect to explore your options and nearby areas that may have homes that fit what you’re looking for.

Sell Your House Before the Holidays

Sell Your House Before the Holidays As you look ahead to the winter season, you’re likely making plans and thinking about what you want to achieve before the year ends. One of those key decision points could be whether or not you want to move this year. If the location or size of your […]

3 Trends That Are Good News for Today’s Homebuyers

3 Trends That Are Good News for Today’s Homebuyers

While higher mortgage rates are creating affordability challenges for homebuyers this year, there is some good news for those people still looking to buy a home.

As the market has cooled this year, some of the intensity buyers faced during the peak frenzy of the pandemic has cooled too. Here are just a few trends that may benefit you when you go to buy a home today.

1. More Homes To Choose from

During the pandemic, housing supply hit a record low at the same time buyer demand skyrocketed. This combination made it difficult to find a home because there just weren’t enough to meet buyer demand. According to Calculated Risk, the supply of homes for sale increased by 39.5% for the week ending October 28 compared to the same week last year.

Even though it’s still a sellers’ market and supply is still lower than more normal levels, you have more to choose from in your home search. That makes finding your dream home a bit less difficult.

2. Bidding Wars Have Eased

One of the top stories in real estate over the past two years was the intensity and frequency of bidding wars. But today, things are different. With more options, you’ll likely see less competition from other buyers looking for homes. According to the National Association of Realtors (NAR), the average number of offers on recently sold homes has declined. This September, the average was 2.5 offers per sale. In contrast, last September, the average was 3.7 offers per sale.

If you tried to buy a house over the past two years, you probably experienced the bidding war frenzy firsthand and may have been outbid on several homes along the way. Now you have a chance to jump back into the market and enjoy searching for a home with less competition.

3. More Negotiation Power

And when you have less competition, you also have more negotiating power as a buyer. Over the last two years, more buyers were willing to skip important steps in the homebuying process, like the appraisal or inspection, to try to win a bidding war. But the latest data from the National Association of Realtors (NAR) shows the percentage of buyers waiving those contingencies is going down.

As a buyer, this is good news. The appraisal and the inspection give you important information about the value and condition of the home you’re buying. And if something turns up in the inspection, you have more power today to renegotiate with the seller.

A survey from realtor.com confirms more sellers are accepting offers that include contingencies today. According to that report, 95% of sellers said buyers requested a home inspection, and 67% negotiated with buyers on repairs as a result of the inspection findings.

Bottom Line

While buyers still face challenges today, they’re not necessarily the same ones you may have been up against just a year or so ago. If you were outbid or had trouble finding a home in the past, now may be the moment you’ve been waiting for. Let’s connect to start the homebuying process today.

Taking the Fear out of Saving for a Home

Taking the Fear out of Saving for a Home If you’re planning to buy a home, knowing what to budget for and how to save may sound scary at first. But it doesn’t have to be. One way to take the fear out of budgeting is understanding some of the costs you might encounter. And […]

Applying for a Mortgage Doesn’t Have To Be Scary

Applying for a Mortgage Doesn’t Have To Be Scary [INFOGRAPHIC]

Some Highlights

Even with higher mortgage rates, the mortgage process doesn’t need to be something you fear. Here are some steps to help as you set out to buy a home.

Know your credit score and work to build strong credit. When you’re ready, lean on the pros and connect with a lender so you can get pre-approved and begin your home search.

Any major life change can be scary, and buying a home is no different. Let’s connect so you have an advisor by your side to take fear out of the equation.