By Mike Lentz | The Mike Lentz Team – Keller Williams Realty

Most first-time buyers don’t put 20% down. The national median is just 10%, and many qualified buyers use loan programs requiring 3.5% or even 0% down. With median prices ranging from $290,000 in Salem County to $415,000 in Burlington County, understanding your actual down payment options can help you buy years sooner than you thought possible.

According to Google Trends, online searches for down payment information recently hit an all-time high. More buyers are trying to figure out what they really need to save before making a move (see graph below):

If you’re wondering the same thing, you can turn to the internet for answers. But it’s better to ask a local expert. Because here’s what a pro would tell you.

The 20% Down Payment Myth

The idea that you need 20% down to buy a home is one of the biggest misconceptions around the homebuying process. The data debunks the myth.

While there are benefits to putting that much money down, most first-time buyers put down far less.

Here’s why. Unless it’s stated by your lender, you typically don’t have to have a 20% down payment. There are loan options designed to help you get into a home with a much smaller upfront cost. As the Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry – there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .“

For example, FHA loans allow down payments as low as 3.5%. VA and USDA loans offer zero down payment options for qualified applicants, like Veterans.

Those options are just one reason so many first-time buyers are able to buy without a 20% down payment.

What Buyers Are Actually Putting Down

So, if buyers aren’t doing 20%, how much do they actually put down?

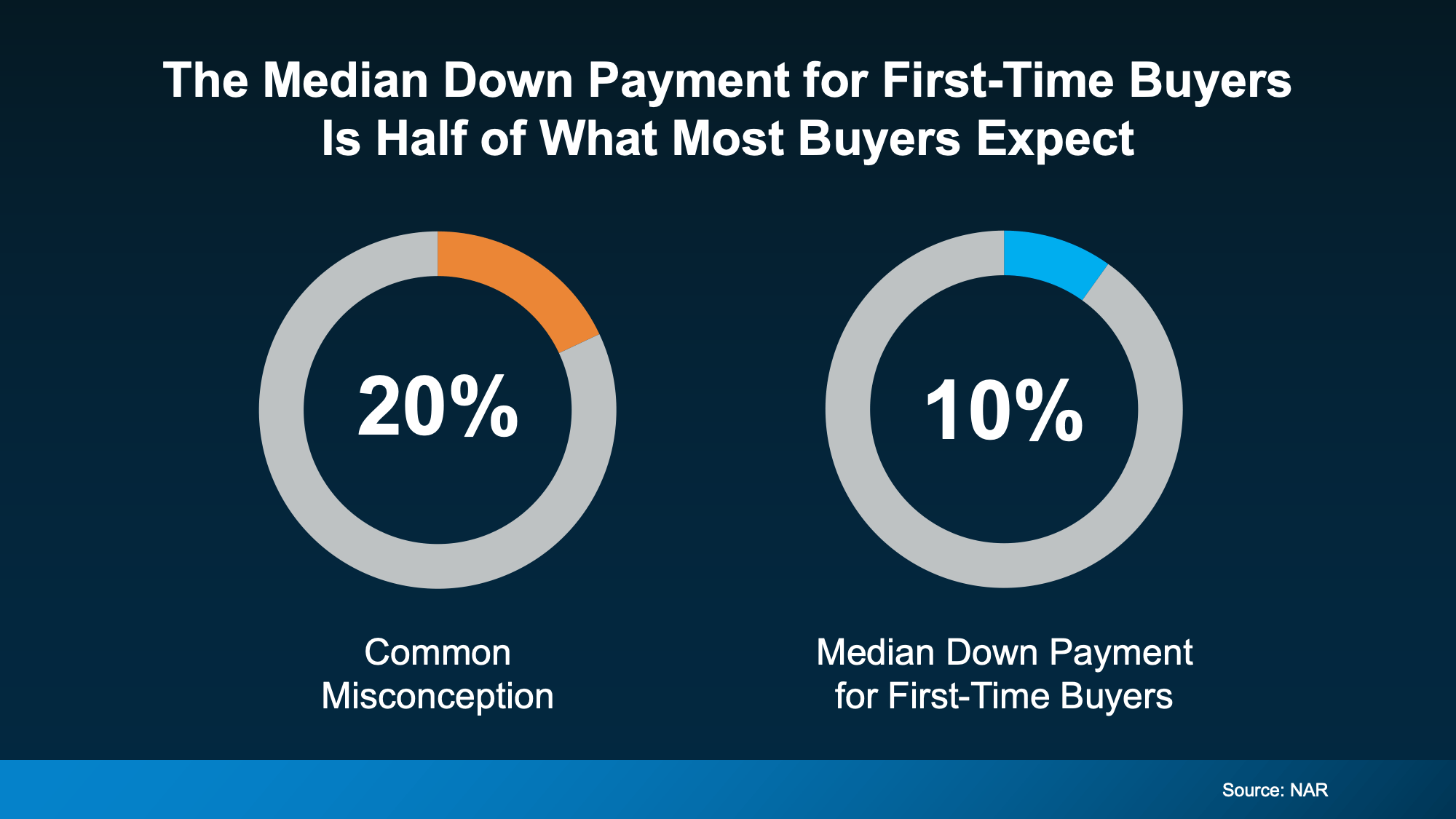

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is only 10%. That’s half of what you probably expected.

That means if you’re aiming to save 20% because you think you have to, you may be setting a timeline that’s longer than necessary.

How This Applies Locally

Median prices across South Jersey vary by county. In Camden County, the median hit $350,000 in March, up 6.4% year-over-year. Burlington County reached $396,000, posting a 2.7% annual gain. Gloucester County climbed to $365,000, up 5.2%.

A 10% down payment on these medians means $35,000 in Camden County, $39,600 in Burlington County, and $36,500 in Gloucester County. That’s dramatically less than the $70,000 to $80,000 you’d need at 20%.

With homes averaging just 22 to 26 days on market across the region, having your down payment ready matters. But it doesn’t need to be as high as you think.

Why You Should Look into Down Payment Assistance Programs

There are programs designed to help you save for a down payment. They can make a big difference in how fast you hit your savings target. Unfortunately, buyers don’t realize how many there are, or that they may qualify for help.

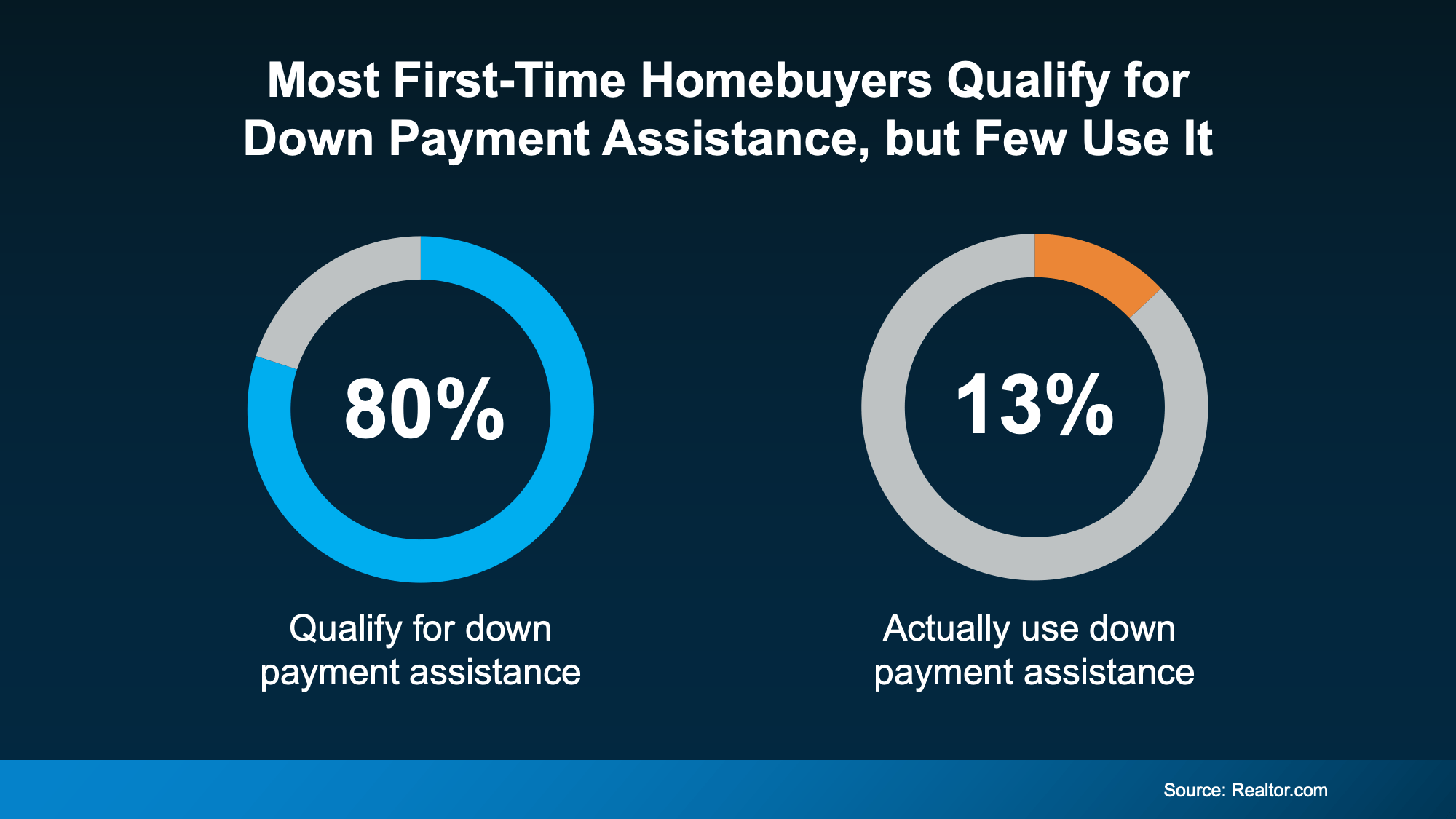

Research from Realtor.com shows almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% actually use it (see chart below):

That’s a big miss holding would-be buyers like you back.

In the U.S., there are over 2,600 homeownership programs available. Many offer significant financial support. As Down Payment Resource shares:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.“

Imagine how much further your savings could go with an extra $18,000 you can use to buy. In some cases, you may even be able to stack multiple programs. That gives what you’ve saved an even bigger boost.

New Jersey offers state-specific programs through the New Jersey Housing and Mortgage Finance Agency (NJHMFA). These programs provide grants and low-interest loans to qualified first-time buyers. Combined with the region’s strong inventory gains – Camden County added 42% more active listings year-over-year – assistance programs open doors that felt locked just months ago.

Local Market Momentum Favors Prepared Buyers

The South Jersey market showed remarkable balance in March. While sales dipped modestly across all five counties, pricing held firm or climbed.

In Camden County, 426 homes closed with 64% commanding asking price or better. Burlington County closed 385 sales, with 60% at or above list. Gloucester County saw 66% at or above asking despite an 16% sales decline.

Speed remains the defining characteristic. Homes averaged 26 days on market in Camden County, 22 in Burlington County, and 24 in Gloucester County. Well-priced properties disappear before many buyers even schedule showings.

If you’re stuck believing you need 20% down, you’re giving other buyers a head start. The gap between what you think you need and what you actually need could represent years of unnecessary waiting.

Bottom Line

Most first-time buyers don’t put 20% down. If you’ve been waiting to buy until you have that saved, you may be setting a timeline that’s longer than necessary.

To find out what you really need to save and if you qualify for any help, connect with a trusted lender. They can walk you through your options. You may be able to buy sooner than you thought.

If you want to talk through what this means for your situation, schedule a quick call and we’ll walk through it together.

For the full picture in your county, see our latest recaps for Camden, Burlington, Gloucester, Salem, and Cumberland Counties.