By Mike Lentz | The Mike Lentz Team – Keller Williams Realty

For most first-time buyers in this market, yes. The average federal refund this year is up 11.1%, which can be the difference between closing in 2026 and waiting another year. Applied to a down payment, closing costs, or a rate buy-down, a refund of $3,000 to $5,000 compounds into meaningful savings over the life of a loan.

For first-time buyers weighing a purchase this spring, a tax refund down payment is one of the fastest ways to shorten the timeline. Most households in Gloucester, Camden, and Burlington counties do not stumble at the mortgage qualification step. They stumble on the cash needed up front. A few thousand dollars of refund money, applied correctly, often closes that gap.

The useful question is not whether to use your refund. It is where it does the most work for the deal you are actually running. The answer depends on the price point, the lender, and the structure of your offer. Here is how we think about it at the kitchen table with buyers.

Refunds Are Larger This Year

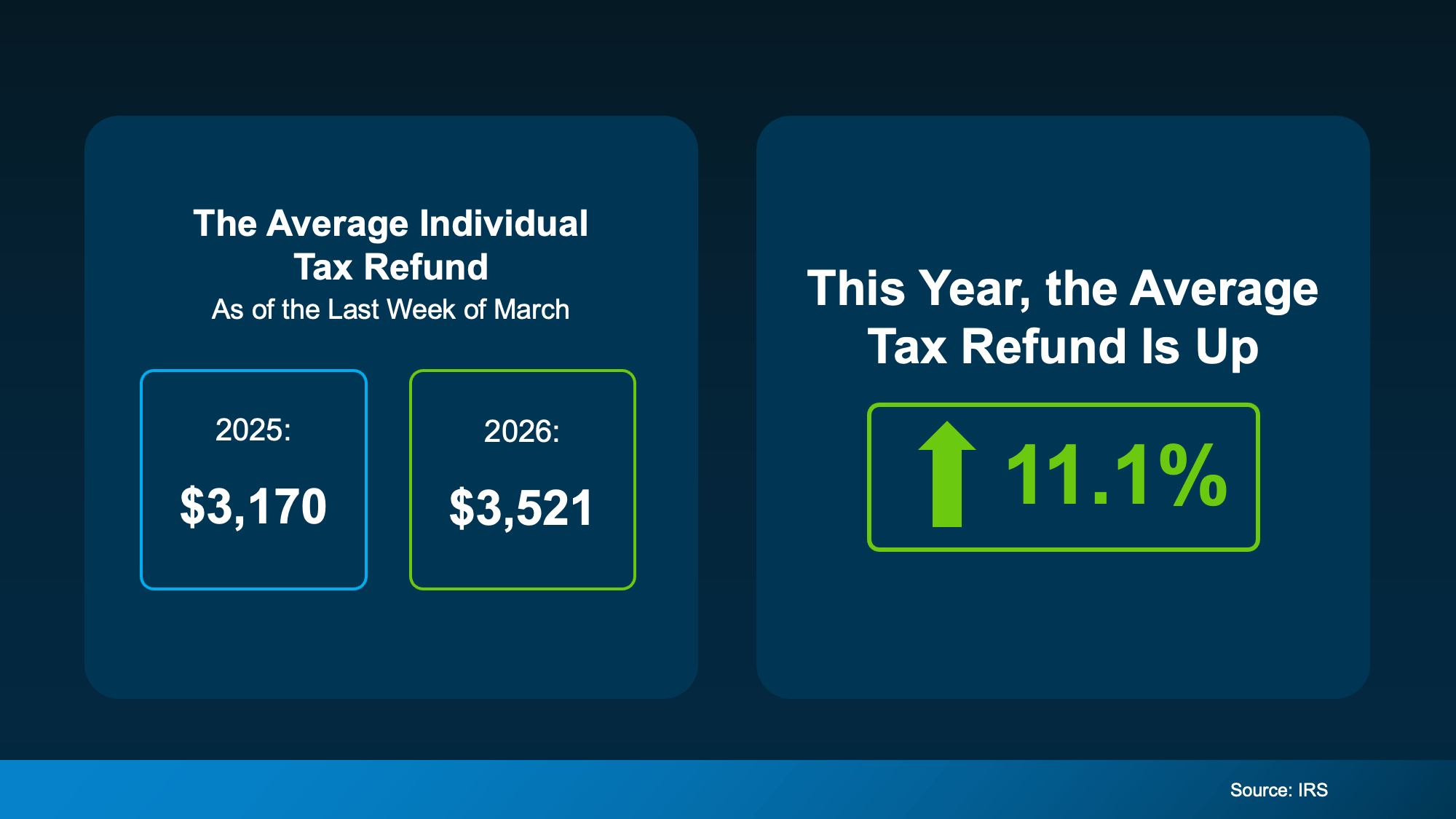

The IRS reports the average individual refund through late March 2026 is 11.1% higher than last year. For context, that moves a typical $3,200 refund closer to $3,550. For households claiming the Earned Income Tax Credit or the Child Tax Credit, the check is often larger.

Your number will differ. What matters is that for most buyers in our price band, the refund arrives at the exact point in the year when the spring and summer listings hit the market. That timing is not accidental, and it is worth planning around.

Option One: Tax Refund Down Payment

The most common use of refund money is adding it to a down payment. For South Jersey buyers, this is usually the move with the highest impact. Here is why.

Most first-time buyers in New Jersey are using either an FHA loan (3.5% down) or a conventional loan with 3% to 5% down. A home in Glassboro or Pitman priced at $325,000 requires roughly $9,750 to $16,250 at the minimum down payment levels. A refund of $3,500 to $5,000 closes a meaningful part of that gap, or bridges the distance between a 3% and a 5% down payment, which can shave the mortgage insurance cost.

One thing worth knowing: the NJHMFA Down Payment Assistance program provides up to $15,000 in a forgivable second mortgage for qualified first-time buyers. Combining that program with refund money is how many of our buyers in Clayton, Blackwood, and Bellmawr actually reach the closing table.

Option Two: Covering Closing Costs

Closing costs in New Jersey typically run 3% to 6% of the purchase price. On a $350,000 home in Sewell or Mantua, that is $10,500 to $21,000 of additional cash needed on top of the down payment. Title insurance, escrows, attorney fees, and lender fees all hit at once, and the number can surprise people.

A tax refund applied to closing costs reduces the amount a buyer has to bring to settlement without reducing their cash reserves. That matters because most lenders want to see several months of reserves after closing, not zero dollars in the account the day after keys change hands.

In a negotiated offer, it is sometimes possible to ask the seller for closing cost credits, which shifts that burden. In 2024 and 2025, seller concessions were nearly unheard of in most of South Jersey. In 2026, the picture is mixed. Where multiple offers are still in play, concessions are rarely possible. Where inventory is sitting for a little longer, they are back on the table.

Option Three: Buying Down the Rate

The third use is a rate buy-down. On a 30-year mortgage, one discount point costs 1% of the loan amount and typically lowers the rate by 0.25%. On a $300,000 loan, one point is $3,000 and usually saves $45 to $55 a month, depending on the exact rate environment.

The arithmetic only favors a buy-down when a buyer plans to stay in the home long enough to recover the upfront cost. For South Jersey buyers who intend to stay five years or more, that break-even is usually around year four to five, and the savings compound every month after that.

A temporary 2-1 buy-down is a different tool. It lowers the effective rate for the first two years of the loan, which is useful when a buyer expects income growth in that window or when the offer includes seller-paid buy-down credits. We run the numbers both ways for buyers before recommending one over the other.

Where a Refund Goes the Furthest in South Jersey

Not every market responds to refund money the same way. In Gloucester County towns like Deptford, Woodbury, and Williamstown, entry-level homes in the $275,000 to $400,000 range are still the majority of inventory. A $4,000 refund applied to a down payment on those homes is meaningful.

In Camden County, Cherry Hill, Voorhees, and Collingswood run higher, typically $425,000 to $750,000+ for single-family homes. On those prices, refund money works harder as closing-cost coverage or a temporary buy-down than as down payment.

In Burlington County, Mount Laurel and Marlton sit in between. Delran offers more inventory in the $400,000 to $500,000 range, which tends to be where refund-plus-NJHMFA combinations produce the strongest offers.

Cumberland and Salem counties still offer the most accessible entry points in the region, with single-family homes in Vineland and Pennsville frequently available under $275,000. A refund covers a significant portion of the required cash in that price band.

What We Tell Buyers Before They Deploy the Refund

Three questions we work through with buyers before moving refund money into a purchase:

- Is your emergency fund already built? Closing a home with zero reserves is a problem. Lenders require reserves, and life requires them more.

- Is any high-interest debt outstanding? A 22% credit card balance usually beats a 6.5% mortgage for where the dollar should go first.

- Is your closing timeline within 90 days? If yes, the refund is best held as liquid cash for the specific closing. If not, consider parking it in a high-yield savings account until the deal is identified.

Most agents will not ask those questions. They are not comfortable recommending someone wait another cycle. We do not share that discomfort. The buyers we work with stay with us for twenty years because we treated the first transaction like the long-term decision it was.

Bottom Line

A tax refund down payment, or a refund used for closing costs or a rate buy-down, can shorten the path to homeownership in South Jersey by six to twelve months for the right buyer. The key is matching the dollar to the biggest constraint in the deal.

If you have a refund coming and want to know exactly how far it stretches in your target price range, schedule a 20-minute call. We will run the math with your lender’s pre-approval numbers and tell you what moves actually work. If the timing is not right yet, we will tell you that too.