By Mike Lentz | The Mike Lentz Team – Keller Williams Realty

On average, homeowners carry 43 times more net worth than renters. Buyers who closed in Gloucester, Camden, and Burlington counties five years ago are sitting on meaningful equity today. Renters in the same markets have nothing comparable to show for the same five years of monthly payments.

The question we hear most often from South Jersey renters is direct: is it even worth trying to buy right now? With current home prices and mortgage rates, renting can feel like the easier path, and for some households it is the right call for the moment. The part of the renting vs. buying in South Jersey decision that does not get enough air time is what each choice does to your net worth over the next ten years. That is the conversation we want to have here, using the numbers rather than the usual talking points.

What Renting Actually Gets You

Renting has real advantages worth naming plainly:

- Lower upfront costs

- No responsibility for maintenance or major repairs

- Flexibility to relocate on a short timeline

Those are not small things, particularly for a household in transition, a recent graduate, or someone expecting to leave the region within a year or two. Renting is a legitimate financial choice in the right circumstances.

At the same time, a Bank of America survey found 70% of aspiring homeowners worry about what long-term renting means for their future. That concern is consistent with what Yahoo Finance put plainly:

“Paying rent doesn’t build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

Renting delivers a roof. It does not deliver an asset. Both things can be true.

The Equity Gap Between Renting and Buying in South Jersey

Homeownership is one of the most consistent wealth-building tools available to American households. The mechanism is straightforward. Every month, part of your mortgage payment goes toward principal, which reduces what you owe. At the same time, home values tend to appreciate over multi-year horizons. Those two forces stack on top of each other and compound.

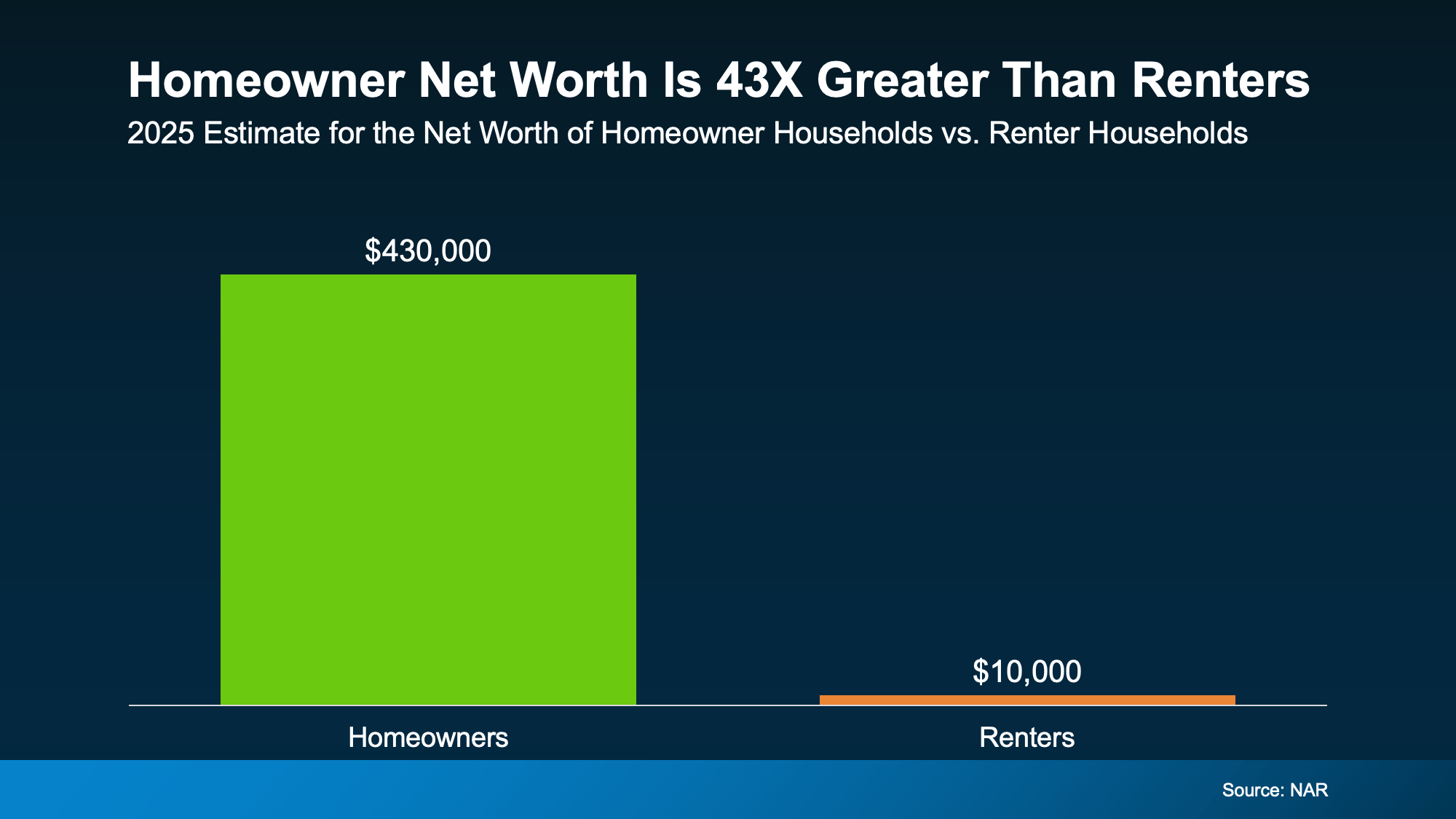

The National Association of Realtors reports the average homeowner’s net worth is 43 times greater than the average renter’s.

The national medians are stark:

- Homeowners: $430,000 median net worth

- Renters: $10,000 median net worth

That gap is not about lifestyle choices or income differences. It is a direct result of where the monthly check goes. One path builds an asset you own. The other builds an asset your landlord owns.

Why the Wealth Gap Keeps Widening

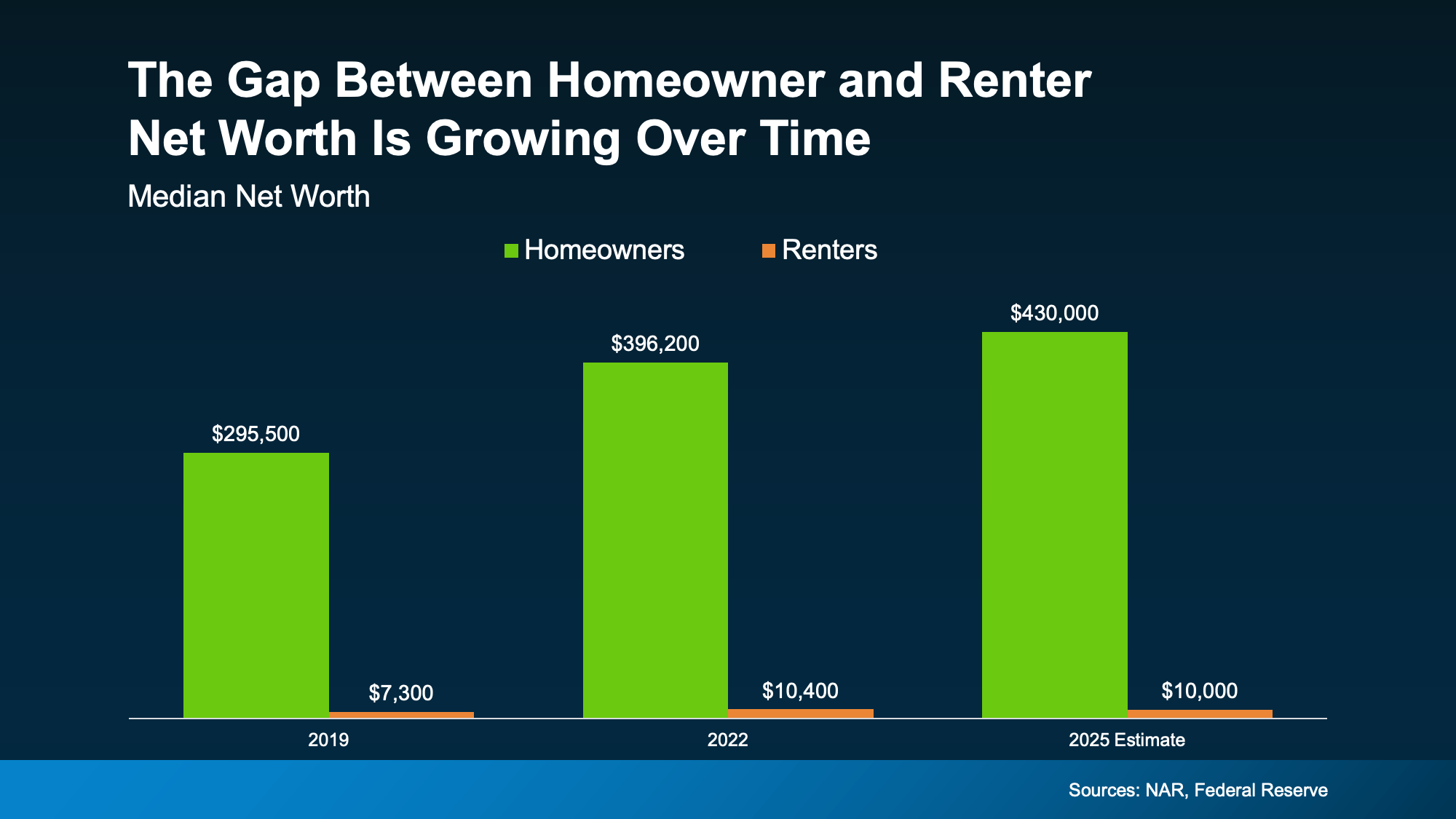

The more useful data point is the trend. Every net worth report from the Federal Reserve and NAR over the last decade shows the gap between owners and renters expanding, not closing.

Even in 2025, when home prices moderated nationally, homeowners still added ground. In South Jersey specifically, we have tracked buyers who closed in Washington Twp Deptford, Mount Laurel, and Moorestown three to five years ago. Several of them are sitting on six-figure equity positions today from appreciation alone, before you count the principal they have paid down. That is not a projection. That is what already happened in the counties we work in every week.

A Simple 10-Year Renting vs. Buying Comparison

Consider a common South Jersey scenario. A household is weighing renting a three-bedroom home in Sewell for $2,600 a month against buying a similar property for $375,000 with 5% down and a 30-year mortgage. After 10 years of renting at typical 3% annual rent increases, the household has paid roughly $358,000 in rent with zero equity to show for it. After 10 years of owning the same property, the household has paid down approximately $65,000 in principal. At a conservative 3.5% average annual appreciation, which is below the recent Gloucester and Camden County pace, the home is worth roughly $530,000.

Net worth gain from the home alone in that decade: around $220,000, before counting any tax benefits. The monthly out-of-pocket difference during those years is usually smaller than people expect once property tax deductions, principal paydown, and rent escalations are factored in. That is where the 43-times wealth gap actually comes from. It is not magic. It is straightforward math that runs for ten years.

Where the Math Pencils Out for South Jersey Buyers

One advantage South Jersey has over most of the Philadelphia metro is entry pricing that still works on a single middle-class income. A first-time buyer looking in Glassboro, Mantua, or Williamstown can find single-family homes in the $300,000s. In Cherry Hill and Mount Laurel the numbers climb, but buyers who commit to a five-year horizon typically come out ahead of what they would have paid in rent.

First-time buyers in New Jersey also have tools renters do not:

- The NJHMFA First-Time Homebuyer Mortgage offers below-market rates through participating lenders.

- Down Payment Assistance of up to $15,000 is available through NJHMFA for qualified buyers.

- New Jersey property tax deductions and the Homestead benefit apply once you are an owner.

None of those programs exist for renters. They are one of several structural reasons the wealth gap keeps widening over time.

When Renting Is Still the Right Call

Buying is not always the right move, and we say that to prospective clients regularly. There are situations where renting for another year or two is the honest answer:

- A timeline under three years in the same region

- Unstable or commission-based income without a track record

- High-interest consumer debt that would be better retired first

- An emergency fund that is not yet built

Most agents will not talk anyone out of a purchase. We will, when the numbers do not work. Our job is not to find a commission. It is to give you the data and let you make your own decision.

If you plan to stay in South Jersey for at least five years, have stable household income, and can cover a reasonable down payment and closing costs, the math almost always favors buying. If you cannot check those boxes yet, the right work is building toward them, and a good agent should help you see that timeline clearly.

How to Think About Renting vs. Buying in South Jersey

The useful comparison is not rent vs. mortgage payment in month one. It is net worth in year ten. When you run the numbers that way, including principal paydown, appreciation at historical South Jersey rates, and tax treatment, the renting vs. buying in South Jersey gap is rarely close. The real question is whether the timing works for your specific situation, not whether buying is worth it in general.

Two resources that help with that conversation:

- Our rundown on how the renting and buying math has shifted recently

- Our list of five questions every South Jersey buyer should answer first

Bottom Line

Renting can feel easier in the current month. Over a ten-year window, it usually costs more. Not in monthly payments, but in the net worth a household walks away with at the end.

The first step for anyone weighing renting vs. buying in South Jersey is a conversation about your specific timeline, numbers, and goals. Schedule a 20-minute call and we will run the math with you. If buying makes sense, we will build a plan. If it does not yet, we will tell you exactly what it takes to get there.