By Mike Lentz | The Mike Lentz Team – Keller Williams Realty

Yes, carrying student debt doesn’t automatically disqualify you from getting a mortgage. Lenders evaluate your debt-to-income ratio, which includes all monthly debt payments, not just student loans. In fact, one-third of first-time homebuyers across South Jersey and nationwide purchased homes while still carrying student loan debt.

The relationship between student loans and homeownership is back in the spotlight. Whether you’ve been following the headlines or just catching updates here and there, they’ve likely been on your mind. And if you’re wondering whether you need to pause your plans to buy a home, here’s what you need to know.

Having student loans doesn’t automatically mean buying a home has to wait.

The Biggest Myth About Student Loans and Homeownership

One of the most common misconceptions among first-time buyers is believing they must pay off their student loans before qualifying for a mortgage. But in most cases, that’s simply not true.

Student loans typically get evaluated the same way other debts do, like credit cards or car payments. As an article from Redfin explains:

“Yes, you can get a mortgage with student loan debt. Lenders primarily assess your debt-to-income (DTI) ratio, which compares your monthly debt payments, including student loans, to your gross monthly income. Having student debt doesn’t automatically disqualify you if your DTI is within acceptable limits.”

So having that loan on your credit report isn’t some special red flag that immediately disqualifies you.

Instead, lenders look at your overall financial picture. That includes your income, credit history, employment stability, and more. Student loans are one piece of that puzzle, but they’re not the entire picture.

You’re in Better Company Than You Think

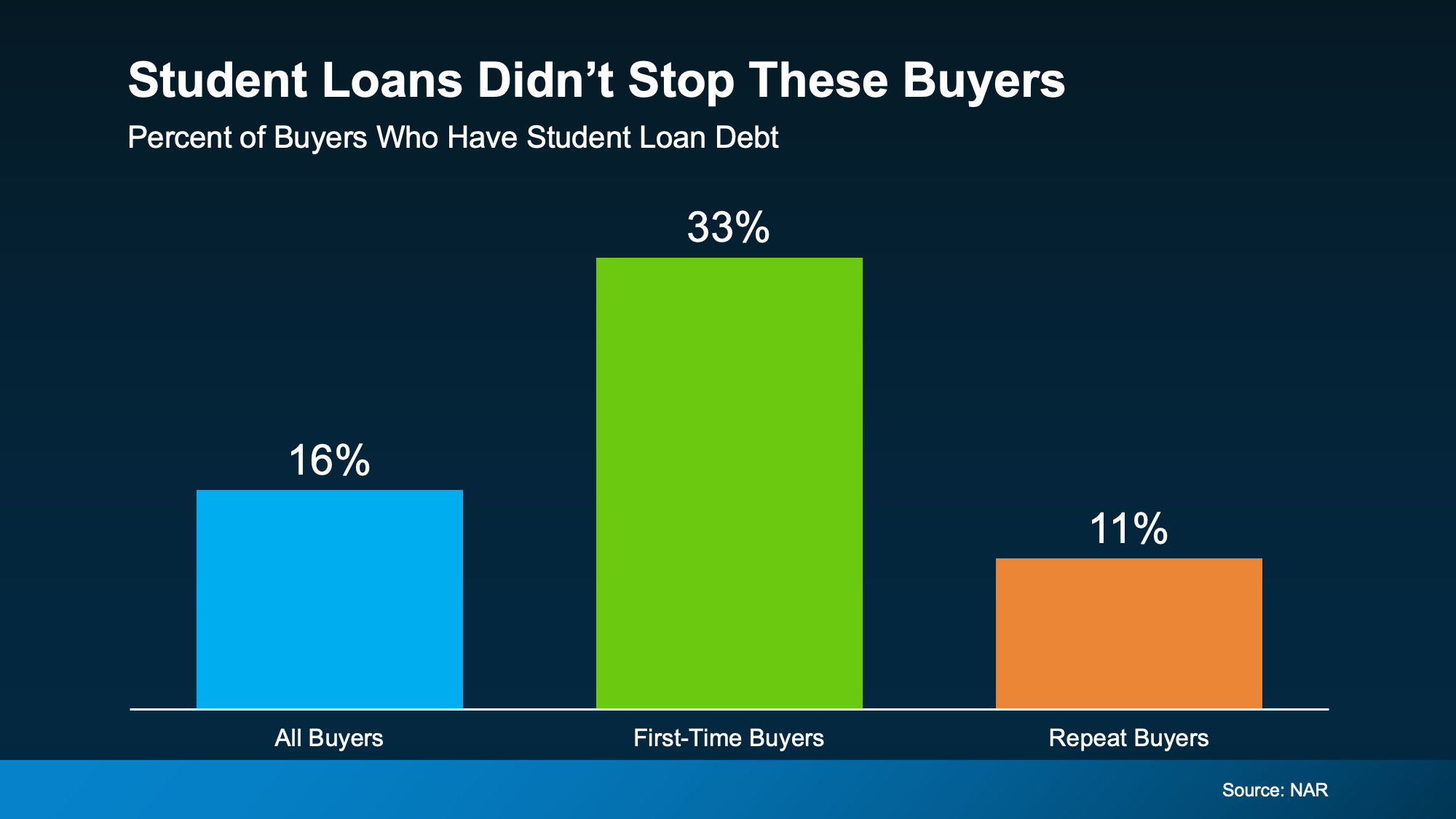

Here’s a stat from the National Association of Realtors (NAR) that proves you can have student debt and still buy a home. Their research shows 33% of first-time homebuyers still had student loan debt.

That’s 1 out of every 3 first-time buyers. The median amount they owed? $30,400.

Let that reassure you. People are buying homes with student debt every single day across Camden, Burlington, Gloucester, Salem, and Cumberland counties. The path to homeownership is still open even when carrying student loans.

How Lenders Evaluate Student Loans and Homeownership Applications

When you apply for a mortgage, lenders calculate your debt-to-income ratio. That’s your total monthly debt payments divided by your gross monthly income. Most lenders want to see a DTI below 43%, though some loan programs allow higher ratios.

Your student loan payment counts toward that calculation. But so do your car payment, credit card minimums, and any other recurring debt. If your income is strong enough to keep your DTI in an acceptable range, you can qualify.

This is exactly why talking to a lender early matters. They can run your actual numbers and show you what you qualify for based on your real situation, not assumptions.

Don’t Count Yourself Out Before You Even Try

Here’s where a lot of buyers trip themselves up. They assume the worst and never even check what they could actually qualify for. But your situation is more unique than a blanket “no.”

If your income is steady and the rest of your finances are in decent shape, buying a home could be more realistic than you think. The only way to know for sure is to actually run the numbers with someone who does this for a living.

You may discover you’re closer to buying than you think. And if you’re not quite ready yet, a lender can give you a clear roadmap showing exactly what needs to improve and by how much.

What You Can Do Right Now

Start by getting pre-qualified. It’s free, it doesn’t hurt your credit, and it gives you a realistic picture of where you stand. Bring documentation of your income, debts, and credit history.

If your DTI is too high, ask what steps would help. Sometimes it’s as simple as paying down a credit card or increasing your income slightly. Other times, you might already qualify and just didn’t realize it.

Either way, you’ll have real information instead of guessing. And real information leads to better decisions.

Bottom Line

The connection between student loans and homeownership doesn’t have to be a roadblock. If you’ve been putting off your homebuying plans because of that debt, talk to a lender about your options. It may not be the barrier you think it is.

If you want to talk through what this means for your situation, schedule a quick call and we’ll walk through it together.

For the full picture in your county, see our county market reports for Camden, Burlington, Gloucester, Salem, and Cumberland counties.