By Mike Lentz | The Mike Lentz Team – Keller Williams Realty

Most Veterans don’t realize VA home loan benefits include zero down payment options, reduced closing costs, and no private mortgage insurance requirements. These advantages don’t eliminate the competition in South Jersey’s housing market, but they remove several financial barriers that stop Veterans from even getting to the table.

Nearly half of Veterans (49%) feel homeownership is currently out of reach, according to a recent survey from NewDay USA. But many are closer than they think, especially when they understand the full scope of VA home loan benefits available to them.

If you’re a Veteran in Camden, Burlington, Gloucester, Salem, or Cumberland counties, you probably know the Veterans Affairs (VA) home loan benefit exists. It’s been around for over 80 years. What you might not know is what it actually covers.

Three misconceptions trip up Veterans the most:

Any one of those beliefs could be holding you back. Let’s walk through all three, so you have the information you really need.

Understanding VA Home Loan Benefits: Zero Down Payment Options

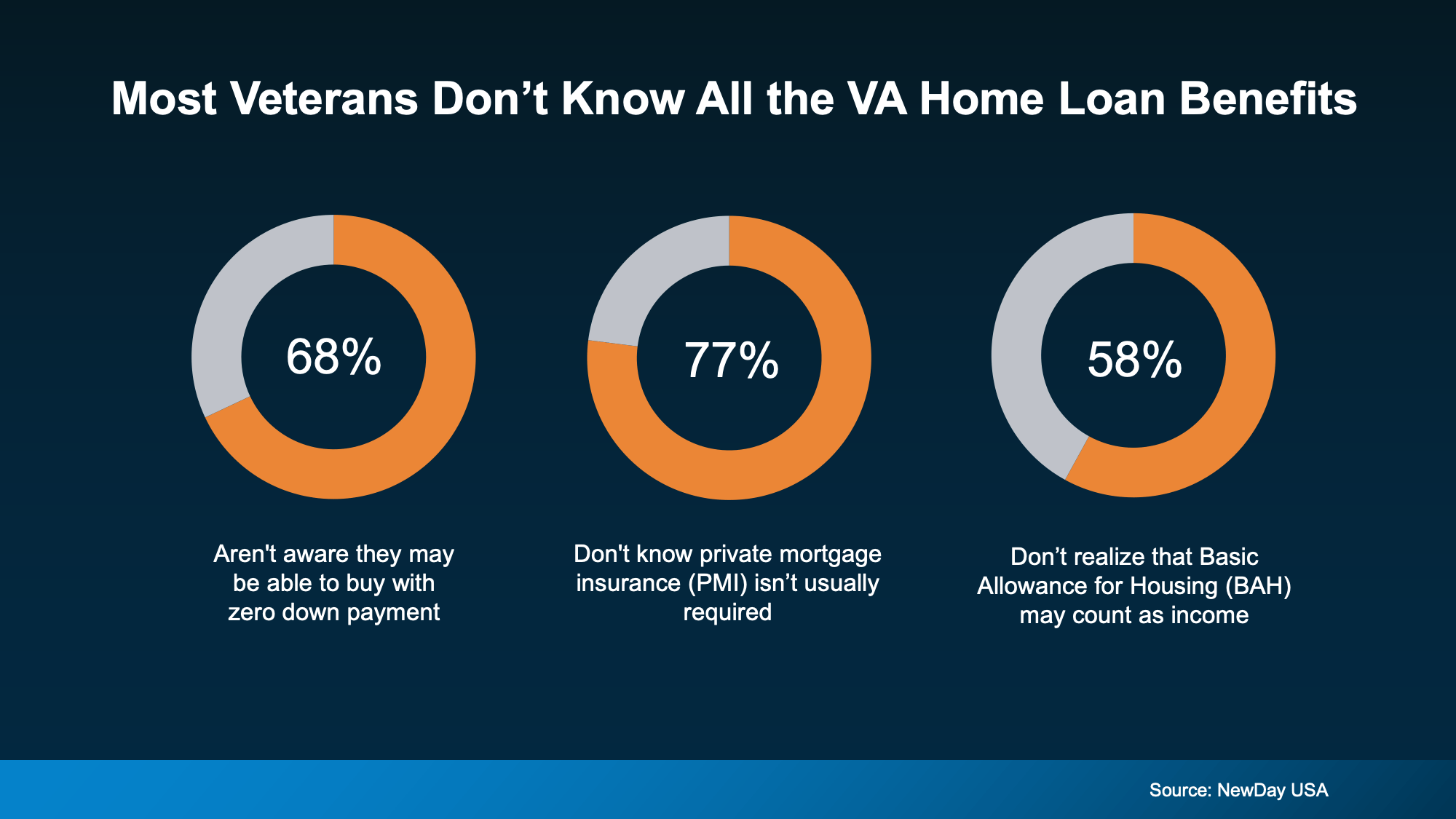

The potential to put zero money down is probably the biggest perk of a VA loan. But most homebuyers don’t even realize that’s an option.

According to the NewDay USA survey, many respondents guessed they’d need to save somewhere between $10,000 and $19,900 before they could buy. That’s years of saving for an upfront cost that isn’t always required.

For Veterans in Burlington County where the median home price sits at $392,500, or Gloucester County at $370,000, that zero down option removes a major barrier. You don’t have to wait years to save for a down payment before you start looking.

Lower Closing Costs With VA Home Loan Benefits

According to the Department of Veterans Affairs, with VA loans, there can be limits on the types of closing costs buyers have to pay.

That means more money stays in your pocket on closing day. And you have less to save up for before you can buy.

The benefit combined with the down payment perk can speed up your buying timeline. In Salem County where the median price is $270,000 or Camden County at $369,990, lower closing costs help.

No Private Mortgage Insurance Required

Unlike many other loan options, VA loans typically don’t require private mortgage insurance (PMI). This applies even with low or no money down.

If you take out a conventional loan instead, you could pay $100 to $300 a month in PMI until you hit 20% equity, according to NewDay USA. Over time, that’s a difference of thousands of dollars.

BAH and BAS May Boost Your Qualification Amount

If you’re on active duty or if you’re a qualifying reservist, your Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS) may count toward income qualification on a VA loan.

So if you were running the numbers without factoring your BAH or BAS in, you could qualify for more than you thought. Both BAH and BAS are non-taxable, so they can help raise the amount you can qualify for.

This matters when inventory is limited. In Burlington County, for example, new listings dropped 39% to 530 homes in April. Being able to qualify for more gives you additional options.

What The Market Actually Looks Like For VA Buyers Right Now

We need to be direct about this: South Jersey is still a competitive market. VA loan benefits give you real advantages, but they don’t make buying easy.

In Camden County, 49.5% of buyers paid over list price in April. That’s down from 61.2% a year ago. In Gloucester County, 44.4% closed above asking versus 51.4% the previous year. The trend is better. But nearly half of all buyers still paying above asking price is not a relaxed market. If you’re shopping, expect competition.

Homes are sitting slightly longer. Camden County averaged 17 days on market. Burlington County averaged 18. A year ago, some of these properties moved faster. That extra time helps, but we’re not talking about weeks of breathing room. You still need to be prepared and ready to act.

Inventory did improve. Camden County climbed 15.6% to 856 active listings. Gloucester County increased 13.3% to 602 properties. More options than last year. Still not enough to tip the balance toward buyers.

So where does that leave Veterans with VA loans? In a better position than most buyers, because your financing costs are lower from day one. Zero down and no PMI mean you keep more cash in reserve. That matters when you’re competing against other offers and need flexibility on inspection terms or closing timelines. It’s an edge. Not a guarantee.

For more context on how conditions affect buyers, see our guide on the current buyer’s and seller’s market.

Taking the Next Step

VA home loans remove real financial obstacles. They don’t remove the competition. A trusted lender can walk you through the specifics of what you qualify for and what your monthly costs would look like.

If you’re active duty, you’ve served, or know someone who has, connect with a lender who specializes in VA loans. Get the numbers before you start shopping. In a market this competitive, preparation is the difference between winning a house and losing one. For a full walkthrough of what to know before buying, see our guide on things to know before buying a house.

If you want to talk through what this means for your situation, schedule a quick call and we’ll walk through it together.

For the full picture in your county, see our latest recaps for Camden, Burlington, Gloucester, Salem, and Cumberland counties.